Card, mobile credential, payment and security

In a free on-demand webinar, campus card vendor Blackboard Transact explores the move to student attendance tracking in higher ed and demos its new automated attendance application.

In a free on-demand webinar, campus card vendor Blackboard Transact explores the move to student attendance tracking in higher ed and demos its new automated attendance application.

Automated, card-based solutions for attendance tracking are becoming more common in higher education. Financial aid and other reporting requirements are pushing campuses to track attendance and institutions are striving for ways to increase student success, retention and matriculation.

Blackboard Attendance uses your existing student ID card -- from any campus card vendor – as the tool to track attendance. A small mobile card reader syncs with iOS or Android handsets and tablets to make attendance data available in real time for instructor viewing and future reporting.

It’s cloud-based, SaaS architected and easy to setup and deploy. In this informative webinar, hear Blackboard representatives how institutions and students alike can benefit from automated attendance tracking.

Watch the free, on-demand webinar by clicking here.

It was more than three years ago that US PIRG released its report damning the relationships between financial providers and academic institutions that provided payment card products to students. In its wake, other reports from the agencies like the Government Accountability Office, Congressional hearings and consumer protection efforts followed. Then came the Department of Education's efforts to revamp financial aid disbursement.

The DOE convened a 2014 Negotiated Rulemaking Process to gather input from a cross section of concerned groups. After months of meetings and drafts, negotiators reported that they thought they had successfully re-crafted the rules. But representatives from industry and the consumer advocacy groups failed to reach total consensus, leaving the DOE free to draft the rules as they saw fit.

In mid-May, the DOE’s final proposed rules were released, and they are not favorable for industry, campus administration or even students. They appear to be a win only for the consumer advocacy groups that have been pushing to have banks and payment cards completely removed from the process.

Since the Negotiated Rulemaking began, both the service providers and the campuses relying on them to disburse financial aid to students have been on proverbial pins and needles. The future of this line of business and peripheral services -- such as campus card and bank partnerships that deliver accounts and debit cards to students -- have been up in the air.

I have written about this many times before and have worked with associations, providers and campuses attempting to plan for the future. The goal has been to help the DOE develop productive regulations that protect students and grow these services. But from the beginning, the car has been driven by consumer advocacy bodies that seemed devoted to the banishment of these relationships from higher education.

Still I always believed that cooler heads and data-driven decision making would prevail. After all, I know that the vast majority of these services are beneficial for campuses and students alike – better in most cases because the campus is involved on the student’s behalf.

I kept this cautious optimism throughout the negotiated rulemaking process, loads of phone briefings, several years of conference sessions and a series of draft proposals and comment periods.

I am no longer optimistic.

I fear that the draft regulations released by the DOE in May are likely to pass without significant changes. I have heard no insider intel to suggest that the comment period that ends on July 2 will produce substantive change.

For the first time, this has me thinking about worst-case scenarios. What if the consumer groups get their wish and some or all of these relationships that both campuses and students rely on actually do go away?

As both a student and a university employee, I remember the “net check” process where everyone receiving aid had to get it via paper check. It was painful on both sides. Are we destined to relive it? As other federal programs from Social Security to Veterans Affairs totally eliminate checks, is the DOE pushing campuses backward?

Do they think forcing campuses to manage ACH processes in-house, increase the use of paper checks and push students to use their existing bank accounts really solves a problem students are facing? Many paper checks will be cashed at rip-off payday loan shops. The students’ preexisting bank accounts all charge non-sufficient fund and other traditional fees the DOE is trying to eliminate.

Sadly, many of the products the new regulations will curtail actually are better, as they offer low- or no-fee alternatives that help students access Title IV funds. In the rush to appease the consumer advocates, it seems the DOE has overlooked this reality.

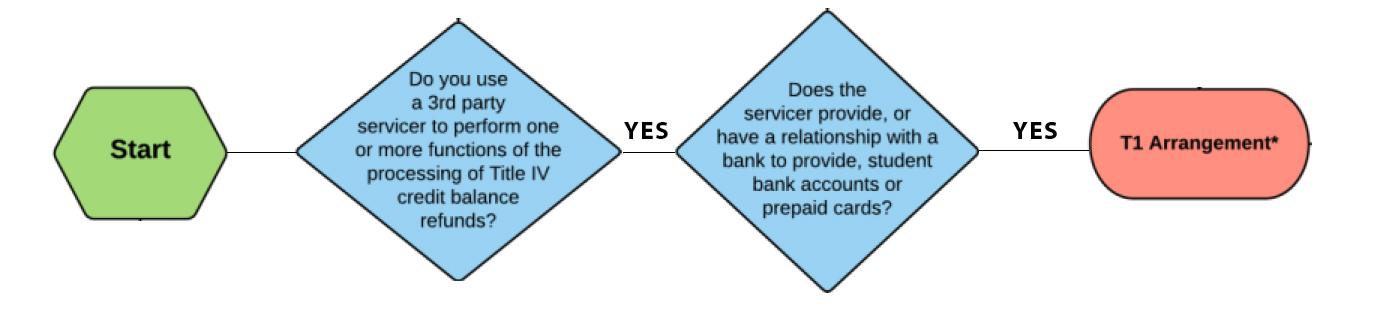

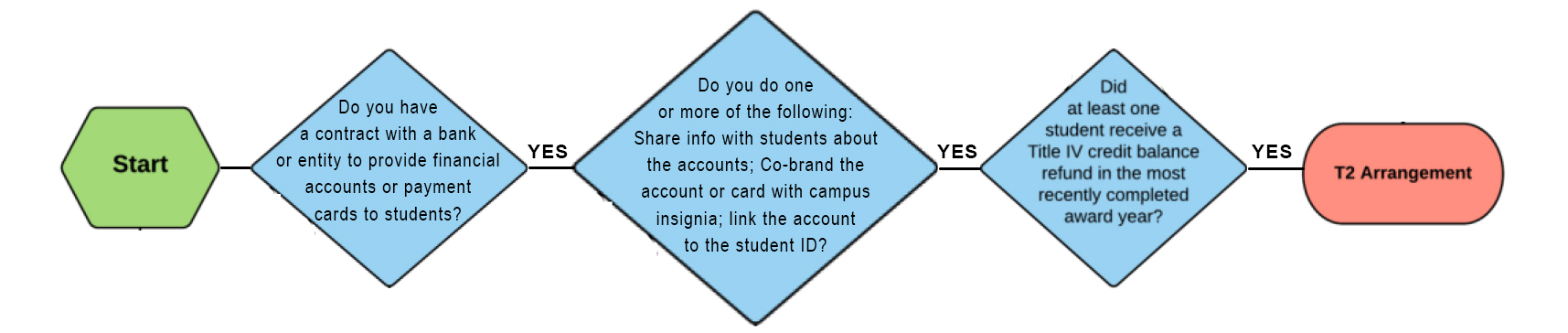

NACUBO created a flowchart to enable a campus to determine whether or not they have a T1 or T2 relationship. In the interest of getting down to layman terminology and simplifying the subject, we have abridged that flowchart to a more basic version.

Do you have a T1 provider?

Do you have a T2 provider?

Lets make some assumptions and head down the path of worst-case scenarios. Assume that the proposed rules pass without substantive change or perhaps get even more punitive toward T1 and/or T2 entities. What might the implication be for your campus?

To state the question another way, “what if my provider goes away?”

A recent US Senate Banking Committee hearing addressed issues that could determine the future of campus card bank partnerships. Though many expected ID cards and aid delivery to be a minor topic in comparison to other Title IV financial aid related issues, it dominated much of the discussion during the hearing titled “Financial Products for Students: Issues and Challenges.”

The following article highlights key testimony, including an opposition letter from the seven Kansas state system institutions, a US PIRG representative outlining the consumer advocate position against these accounts, and finally a banking association president’s case for the positives provided by bank and campus partnerships.

A video of the hearing and testimony is available at the following link. Jump 17:00 minutes into the video coverage to listen in on card-related issues. (http://www.banking.senate.gov/public/index.cfm?FuseAction=Hearings.LiveStream&Hearing_id=8058e98c-2c38-4e5c-999a-fdae0e929bc4)

At the start of the hearing, US Sen. Jerry Moran, R-Kan., read a letter submitted by the presidents of seven institutions in the Kansas state system. It stated their concern with language that regulates any arrangement in which a student opens an account into which the Title IV funds are to be placed.

Senator Moran read from the letter for the Kansas Universities:

“(This regulation) could have a chilling and in some cases terminal effect on good business partnerships that currently benefit students and universities alike.

Students often far from home need access to safe and secure financial services. Financial experience is a necessary part of student life and is essential training in long-term financial health.

Knowing this many schools have signed agreements with banks to provide on-campus financial institutions at low or no cost students. Such services include secure on-campus branches, ATMs, debit cards and financial education programs.

Any regulatory action that could potentially take away students safe convenient and free access to one group of essential services while it simultaneously drives up the cost of education for that same group of students deserves to be studied with extraordinary care.”

Christina Lindstrom, US PIRG spokesperson, highlighted what the consumer group sees as unfair and onerous for students:

“Right now students are being hit with high fees that are hard to avoid as they try to access their federal financial aid refunds through campus sponsored bank accounts and prepaid debit cards. We found in our 2012 report, “The Campus Debit Card Trap,” that two in five college students in the country are exposed to debit cards on campus that may drive up their costs.

Students at some campuses are charged steep and unusual fees to get to their federal financial aid including PIN transaction fees at the point-of-sale, overdraft fees of $37 or more. On the whole these accounts are not necessarily a better deal for students than what they might find through a bank not affiliated with the campus.

Still industry-leading banks and financial firms can see 40-75% of students on a campus using the campus-based product a few years of marketing. How do they do it?

First, banks and financial firms behind these products often rely on multi-million dollar revenue-sharing agreements with campus administrations. The contracts include receiving direct payment to use the school’s logo, providing bonuses for recruiting students and discounted pricing in exchange for marketing access.

In addition they used push marketing and other strategies to steer students into opening up these new accounts over using their existing bank accounts.

Higher One, a prominent financial firm in this market, pre-mails the cards to every student on campus, before they’ve opted in or out. The cards are co-branded with the college logo giving impression that the student must open the account.

At another college, bank representative actually set up tables right outside the student ID office, essentially … aggressively promoting their accounts that students can link to their id cards. Students can get freebies like bags and T-shirts for signing up.

Finally the fees can be high as I mentioned and unusual. Fees on university-sponsored cards include a variety of PIN swipe fees, inactivity fees, overdraft fees, ATM surcharges, fees to reload prepaid cards, fees to check your account balance … I could go on. The fees can be hard to avoid, for example, if a merchant only accepts PIN debit or there’s no fee-free ATM available.

All campus bank accounts and prepaid card services can charge overdrafts. Overdraft coverage is a form of credit since the financial institution covers the consumer shortfall and subsequently repaid the amount extended plus a fee. Some banks engage in the abusive practice of purposefully reordering transactions to maximize overdraft fees. Many banks and financial firms that are playing on campus right now have been held accountable for their abusive practices in this arena.

Overdraft fees are inconsistent with the Department of Education’s existing rules on school-sponsored accounts. Department of Education rules also require that students be provided convenient fee-free ATM access. In practice access can be limited.

One argument that’s being made in defense of these campus banking products is that too many low income students are not able to acquire a bank account other than on campus – these are the unbanked students. The Consumer Financial Protection Bureau found less than one-half a percent of college students in America are legitimately unable to secure a bank account, so new student who comes on the campus without a bank account – she doesn’t have one because she chose not to have one or she hasn’t gotten one yet.

Students do not need campus-sponsored bank accounts.

So I urge you to consider legislation that bans revenue-sharing agreements between colleges and banks or financial firms crafted specifically to offer bank accounts and related banking products to students on campus. The conflict of interest inherent in these accounts is problematic for the student consumer and it needs to be addressed.”

Richard Hunt, President and CEO, Consumer Bankers Association articulates the case for continuation of these relationships and accounts:

Some Consumer Bankers Association members have entered into agreements with institutions of higher education to provide useful services, such as campus ID cards that can be linked, at the option of students, to a standard deposit account. These financial institutions also provide important services, such as on campus financial literacy programs and assistance with financial aid systems to colleges and universities.

According to a GAO report, “Most of the college card fees we reviewed generally were not higher, or in some cases were lower, than those associated with a selection of basic or student checking accounts at national banks. In particular, college card accounts generally did not have monthly maintenance fees, while the basic checking accounts we reviewed typically did.”

Recently, the DOE entered into a negotiated rulemaking with a variety of stakeholders, including students, school representatives, banks, credit unions, consumer groups, and others, on the topic of “cash management,” which includes the disbursement of student aid refunds, federal aid in excess of what is needed to pay school charges. Despite significant progress among non-federal negotiators and the offering of good-faith proposals by the bank and credit union negotiators, consensus proved elusive. This leaves the Department unbound by any agreements worked out during the negotiations, and free to write whatever changes to the regulations it wishes to propose.

CBA shares the DOE’s goal of promoting students’ understanding and management of financial products while ensuring they have meaningful choices. However, we have serious concerns about and objections to the expansiveness of the draft regulation related to disbursement of federal student aid credit balances, particularly with regard to non-disbursement accounts (i.e. accounts opened outside of the Title IV credit balance disbursement process), as well as sponsored disbursement accounts. Similar apprehensions relating to the scope of the DOE’s rulemaking have been expressed by members of both parties and houses of Congress.

With regards to non-disbursement accounts, though the language in the draft regulation presented by the DOE during the negotiated rulemaking is not clear, it would certainly classify as “sponsored accounts” any traditional bank deposit account linked to a “campus card,” such as a college identification card, even though the depository institution offering the account does not facilitate the delivery of federal student aid credit balances for the school – which is the true subject of the rulemaking. In addition, the draft regulation could cover any deposit account that could receive federal student aid credit balance disbursements held by a financial institution that happens to have other types of arrangements with colleges or universities (“educational institutions”). As sponsored accounts, these accounts would be subject to various requirements and significant restrictions under the proposed regulation, impacting relationships that have nothing whatsoever to do with the disbursement of federal student aid credit balances.

While the DOE has authority to write rules concerning Title IV financial aid disbursement and the methods under which disbursements are made, the proposed rule would go beyond that scope and regulate the availability and terms of deposit accounts, including debit cards and prepaid cards, available to students from depository institutions – separate and apart from the financial aid disbursement process. We can identify no authority for DOE’s overreach to regulate deposit accounts that have, at best, only a tangential relationship with those accounts.

Moreover, and more importantly, this broad scope would have a chilling effect on the offering of accounts designed for students and would deprive students of choice and access to valuable, low-cost, and convenient access to bank services, accounts that can be especially useful to those students who arrive on campus without a bank account. For these reasons, we have urged the DOE to reconsider its draft regulation so it does not cover these traditional bank products and services to the extent they are offered outside of disbursement services (i.e., to the extent the deposit account opening process is not integrated within the federal student aid credit balance disbursement process).

In addition to our concerns regarding non-Title IV disbursement accounts and services, we are concerned the proposed regulation will effectively eliminate federal student aid credit balance disbursement accounts — that is, accounts specifically designed to disburse federal student aid credit balances—to the detriment of students and educational institutions.

Federal student aid is disbursed directly to colleges and universities, which use the funds to satisfy a student’s tuition expenses and then disburse the remaining funds to the student to be available for other appropriately related purposes. The DOE has issued a series of student aid credit balance disbursement regulations, which have increased the operational complexity of disbursing these funds to students. Financial service providers have partnered with educational institutions to help these educational institutions satisfy the DOE disbursement requirements. These arrangements enable colleges and universities to reduce the costs of disbursing federal student aid credit balances by utilizing direct deposit, rather than mailing paper checks, thereby decreasing costs for students and schools and provides to students, safe, quick, and convenient access to funds. In some of these arrangements, financial institutions may offer students a deposit account within the credit balance disbursement process itself or, when instructed by the educational institutions, provide them with a prepaid card to access federal student aid credit balances, particularly where a student does not have a pre-existing account to accept a direct deposit of funds. Most importantly, these products and services are always offered as options and are never a requirement. As evidenced by the chart below, institutions of higher education offer students a variety of options for receiving excess student aid funds. Paper checks along with ETFs to a bank account of the student’s choosing are the most prevalent methods for disbursing these funds.

For those students who do not have, or cannot easily access, an existing bank account, a letter from the National Association of College and University Business Officers (NACUBO) notes, “campus banking relationships can streamline the process of establishing a new account or a pre-paid card option provides an alternative to a check.”

The draft regulation presented by the DOE during the aforementioned negotiated rulemaking would effectively deprive students and educational institutions of these services by compelling financial institutions currently providing such “sponsored accounts” – including those in no way opened in connection with the credit balance refund process – to stop providing them to tens of thousands of students on multiple campuses. Draft regulation would restrict nearly all income sources associated with the maintenance and use of these products. With limited or no means to support the cost of providing the services, providers may have no choice but to exit the business and close existing accounts.

The result would be thousands of students losing a convenient, safe, and quick option to access their federal student aid credit balances, and the convenience of a single card that – at the election of the student – can combine financial and school functionality. Payments to students via checks would be more prevalent, especially for those without bank accounts, delaying the students’ access to the funds and potentially causing them to incur off-campus check cashing fees. In addition, it is worth noting the CFPB found that requiring disbursement through electronic fund transfer can reduce fraud and costs.

CBA is hopeful all involved in this process come to understand how banking relationships on campus provide students access to a range of financial products and options to meet their needs. It is especially important that the function of providing general financial services is not adversely affected by concerns over the separate issue of making federal aid funds available to students who wish to have funds deposited directly into a bank account, instead of being given cash or a check.”

CR80News learned that NuVision’s President, Bill Adoff, and Vice President of Sales and Marketing, Brian Adoff, are no longer with the company.

Bill joined the company back in 2001 and has held various roles related to operational management and product development. Brian Adoff joined NuVision in 2007 and served as national sales manager prior to his current role. In response to CR80News’ request for comment, Brian Adoff responded via email.

He said, “although Bill and I have served as the face and driving force of NuVision for the past five-years, we are no longer partnered with NuVision due to differences between ourselves and the other members as to the direction of the company.”

Company representatives have not yet responded to our request for comment.

Researchers lump products, providers together missing the mark

Researchers lump products, providers together missing the mark

As campuses have embraced electronic distribution of financial aid and banking services tied to campus cards, have students been forced to pay more for the convenience? The U.S. PIRG Education Fund says ‘yes,’ suggesting that college students have been unfairly targeted for extra fees to the financial benefit of both banks and universities.

In a June 2012 report entitled “The Campus Debit Card Trap: Are Bank Partnerships Fair to Students?” the U.S. PIRG asserts that university and bank partnerships to offer financial products to students are unfair and should be curtailed. The researchers explore both student ID cards and student loan disbursements that are tied to a bank account, debit card or reloadable prepaid card.

The report states that nearly 900 schools with more than nine million students nationwide have partnerships with banks or other financial firms. These include 32 of the 50 largest public four-year universities, 26 of the 50 largest community colleges and six of the 20 largest private not-for-profit schools. In total, these banking partnerships reach 42% of the student population.

Though the U.S. PIRG contends that universities and financial services companies make a lot of money from these partnerships, not all parties agree.

Most financial institutions working with campus card programs describe long-term relationship building with young, soon-to-be professionals as the driver for these programs. Short-term profit windfalls simply don’t exist, according to representatives from these institutions.

Wells Fargo has relationships with 40 colleges and universities across the country and views college partnerships as a way to teach new users about financial services products. “[We] are being introduced to students, many of who are looking for their first financial institution. We serve their needs, and hopefully they’ll be lifelong customers and build healthy financial habits,” says Richele J. Messick, spokesperson for Wells Fargo.

Most of Wells Fargo’s university partnerships are connected to student ID card services rather than dedicated exclusively to financial aid delivery.

The U.S. PIRG report states that when student ID services become connected to financial options such as open-loop debit cards, it “may mean that a bank/financial aid firm has taken over the process of issuing IDs at the school.”

Wells Fargo contends that this is not the reality of the relationship and that the banking aspect of a student ID is optional. “The student is the one who has the choice,” says Messick. “You don’t have to link a campus ID to a Wells Fargo account.” When the student opts not to turn on the banking feature of an ID, the ID card still contains all the other campus services, but it just doesn’t also function as a debit card.

The main crux of the U.S. PIRG report focuses around fees related to these types of cards as well as debit cards related to student loan disbursements. The report says that universities are increasingly moving to debit cards as a way to give students their loan money, but by using cards as a form of disbursement, students are at risk of incurring fees.

PIRG sees this as a problem when the dollars in question comes from taxpayer-provided grants and federal loans. U.S. PIRG says this money is designed to go to lower income students who can’t afford the fees tied to these accounts.

For a federally funded student loan to be disbursed via a payment card, the Department of Education stipulates that this is possible “as long as the issuing bank provides conveniently located fee-free ATMs.”

The U.S. PIRG report contends that “convenient” and “fee-free” ATMs still cause problems when lines get too long or cash runs out.

It cites that Higher One, a financial aid disbursement firm with agreements at around 520 schools, has 600 ATMs in service. At peak disbursement times, students queue up in long lines to access their money free of charge, and demand can be greater than the supply of money, forcing some to incur fees of up to $5 because they end up using out-of-network ATMs to get their loan funds.

In the case of Higher One’s ATM position, Shoba Lemoine, spokesperson for Higher One, points out that the company’s debit card isn’t the only disbursement option for students. “Once a school contracts with Higher One to help it disburse refunds to its undergraduate population, the students work with Higher One to select how they want their refund.”

With a Higher One account, students may have their refunds sent to them in one of three ways: direct deposit via ACH to any bank of their choice, a paper check by mail or into an optional Higher One OneAccount checking account. “They must actively choose to open this account,” says Lemoine.

“It is absolutely the student’s choice how they want to receive their refund and they will never be charged to receive it, per Title IV requirements. They can also change their preference at any time at no cost to them. This simply gives the student more choice in how they receive their refunds from their school.”

Lemoine says that a student has the option to choose to open a OneAccount FDIC insured checking account for their loan disbursement. Higher One offers this account through its banking partner, and it has no monthly fee and no minimum balance. Students must activate the account themselves and opt to have the loan money deposited into the account. “Approximately 50 percent of students do not choose to open a OneAccount to have their refunds deposited there,” says Lemoine.

In contrast to the report’s portrayal of the students waiting 50 deep in line at a single fee-free ATM on a campus, most providers boast large ATM networks to support student accounts. U.S. Bank has 23,000 ATMs across the country, Wells Fargo has more than 12,000, and both Blackboard and Sallie Mae offer more than 43,000 surcharge-free ATMs via membership in the Allpoint Network.

Blackboard, a long time player in the closed-loop off-campus market with their BbOne offering, launched their financial aid delivery product called BlackboardPay in 2010. The company’s more recent entry gave them a different perspective on financial aid delivery, says Jeff Staples, vice president of market development for Blackboard.

“We committed to deliver a product that best helped students gain access to their Title IV funds,” says Staples. “We looked at the market and asked how we could best serve both the campus and the student … and not at the expense of one over the other.”

Blackboard points to the prepaid platforms from Money Network and Discover as “new tools” they were able to call upon in the creation of the BlackboardPay. These tools provide features they say are not typically found in older debit solutions. According to Staples, BlackboardPay doesn’t charge a PIN debit fee, there is no possibility of overdraft and there are no minimum balance or monthly service fees for active cardholders. Students can access the funds at no cost at more than 7 million Discover merchants, any of the more than 43,000 surcharge-free Allpoint ATMs and via the Money Network Check to any payee including free check-cashing privileges at more than 3,800 Wal-Marts nationwide.

“Seeking technical compliance with Title IV with a few hundred ATMs isn’t really the same as serving the students’ needs with more than 40,000 ATMs plus ATMs deployed on campus,” Staples said.”We think the campus and students deserve the best offering and fee schedule available, not something that’s simply better than average.”

Compelling students to opt for these branded debit cards is another unfair practice, cites the U.S. PIRG report because it opens up students, “already vulnerable as consumers in this area,” to the risk of incurring extra fees, such as hefty overdraft fees and PIN swipe fees.

This may be a young student’s first experience with a financial institution, and the report says that confusing fee structures for these accounts can cost students a lot of money in “hidden” fees.

Most providers of these services take offense to the concept that fees are hidden. Virtually all providers list fees online and provide documentation of fees at multiple points in the process. Financial accounts, like other services, are not free and have fees associated with them. Even “fee-free” accounts have fees for out-of-the-norm activities or improper usage.

“Higher One is not a bank, so cannot speak for those banks named and examined in the study, but Higher One’s offerings do adhere to the fundamental principles discussed by U.S. PIRG in its study, including: 1) providing students with choices, 2) being transparent about how accounts are structured, and 3) enabling colleges and universities to comply with the Department of Education’s standing regulations as they relate to the electronic disbursement of Title IV funds to students,” says Miles Lasater, COO of Higher One in an e-mail statement.

The unfair fees described in the U.S. PIRG’s report are not unlike fees paid by traditional consumers for traditional banking accounts. Virtually all accounts charge for using foreign ATMs and for overdrafting an account. Many banks also charge traditional customers monthly fees for checking accounts. Some banks mitigate those fees for students by offering them accounts with lower fees than the institution’s traditional checking account.

At $3 a month, Wells Fargo’s college checking account is less than its next cheapest account, Value Checking, which costs $9 a month, or $7 for online only statements. Other checking packages that combine savings and debit can cost $12 a month, or $10 for online only statements. The college account includes many benefits of other checking packages, such as checking, savings, a debit card, online bill pay, mobile banking and text account alerts. “Our college offer is a great deal for college students. It’s designed with them in mind,” says Messick.

Higher One’s entry-level checking account has no minimum balance requirements and no monthly fees. It doesn’t require a background check. “Many students find this appealing,” says Lemoine.

Higher One OneAccount customers get a Debit MasterCard, which has a 50-cent fee for PIN-based transactions. “We encourage students to choose free signature-based transactions at the point of sale because they are protected with the MasterCard Zero Liability policy against fraudulent purchases and they are more cost-effective for Higher One. So this fee is avoidable and many students never incur it,” says Lemoine.

Still it is this fee that has caused a great deal of the negative attention to the Higher One offering, and some suggest this has led to the harsh view on student financial account products in general.

“We know that the last thing that a student needs to do is to accumulate more debt,” says Lasater. “We therefore provide financial literacy programs and options so that students can learn how to avoid incurring any fees at all. In short, when it comes to the $1 trillion in student debt that is currently outstanding, we look to be part of the solution in helping students manage their money wisely.”

General purpose reloadable (GPR) cards, commonly called prepaid cards, are a rapidly growing product for campus card and financial aid delivery applications. According to the Federal Reserve, they are also the fastest growing electronic payment method in the U.S. The PIRG reports takes a harsh view of prepaid citing the lack of government regulation and protections.

Describing the prepaid card industry as unregulated, the report cites “no real consumer protections by federal law” and “no protections to limit your liability.”

To the contrary however, bank-issued prepaid products are often treated with the same protections as other payment offerings. Several issuers of prepaid products mentioned in the report, suggest that painting prepaid cards with such as broad stroke is irresponsible and misleading. According to one provider, “it is true that prepaid industry is not regulated in the same way as credit and debit, but as a bank, all our prepaid users are protected in the same way as other card customers.”

Prepaid debit offers great tools as long as the platform is designed with the consumer in mind, says Blackboard’s Staples. “BlackboardPay accounts are FDIC insured and feature an extremely compelling fee schedule,” he adds. “It is a very consumer-friendly iteration of prepaid debit.”

A number of parties – service providers, campuses, associations and publications – have both publicly and privately called into question the accuracy of the PIRG report. Perhaps the most frequently heard compliant was that the report seems to lump all student-facing financial services together. According to a statement issued by the National Association of College and University Business Officers, “the U.S. PIRG report conflates the student aid refund process with debit-linked college and university campus cards.”

In reality, these are very different products. They are marketed differently to students, entered into with different drivers from the institution’s perspective, and priced differently for users.

NACUBO goes on to say the report, “fails to adequately recognize that students have a choice in deciding where and how to manage personal banking and financial transactions and that campus cards are offered by campuses for service, convenience, and security.”

It is difficult to argue that efforts to contain tuition costs require the streamlining of administrative services. This is the fundamental reason that campuses first began to explore electronic delivery of financial aid. According to NACUBO, “the (PIRG) report misleads readers to believe that campuses profit by providing electronic refunds of student financial aid dollars.” Most interviewed for this article agreed that cost savings can be achieved via these services. But they stressed that few campuses create new revenue streams.

Despite the questions surrounding the report’s accuracy, it has already spawned dozens of media reports, legislative rumblings and at least one lawsuit.

U.S. Sen. Dick Durbin, D-Ill., said he “will be working in Washington to put an end to the unreasonable practices highlighted in this (PIRG) report.” The measures he intends to take were not specified in Dubin’s press release.

A lawsuit has been filed, and timing makes it appear to be at least in part a result of the report. A California resident and college student claims financial services provider Higher One “deceptively assessed bank fees” and that the “plaintiff and other Higher One account holders nationwide, were deceived into using a Higher One account in order to access their college financial aid money…then subsequently charged unfair and improperly disclosed bank fees.”

This is not the first time student-facing financial services have come under fire. Most agree it will not be the last. For many professionals that live and breathe these services on a daily basis, it is just unfortunate that some well-intended researchers missed the mark on a number of very fundamental concepts … creating the current stir.

Dates: November 6-8, 2012

Location: Paris, France

Venue: Paris Nord Villepinte Exhibition Centre

URL: http://www.cartes.com

Description: CARTES is the world’s leading Smart Technologies event dedicated to security, payment, identification and mobility. Each year, it brings together 430 exhibitors, 79% of whom come from outside France, 20,000 visitors and 1,300 congress participants to explore the industry’s latest trends and innovations.

Dates: September 18-20, 2012

Location: Tampa, Florida

Venue: Tampa Convention Center

URL: http://www.biometricconference.com/

Description: The 2012 Biometric Consortium Conference and Technology Expo, presented by AFCEA, NIST and NSA, will address the important role that biometrics plays in identification and verification of individuals for government and commercial applications worldwide.

The Conference will be two and a half days of presentations, seminars and panel discussions with the participation of internationally recognized experts in biometric technologies, system and application developers, IT business strategists, and government and commercial officers. The 2012 Conference and Expo focuses on biometric technologies for homeland security, identity management, border crossing, electronic commerce, and other applications.

Dates: March 5-7, 2012

Location: Las Vegas, Nevada

Venue: Mirage Hotel

URL: Click here

Description: CARTES in North America will combine a high level conference program with international experts and a comprehensive exhibition featuring the most representative companies in card manufacturing, payment solutions, identification solutions and digital security.

Mobile devices are poised to become the ID credential of the future. In a recent video interview, Blackboard Transact president David Marr shared his views on mobile platforms in higher ed and the impacts on campus card offices. CR80News’ Chris Corum discussed the topic with Marr as well in a podcast.

Mobile devices are poised to become the ID credential of the future. In a recent video interview, Blackboard Transact president David Marr shared his views on mobile platforms in higher ed and the impacts on campus card offices. CR80News’ Chris Corum discussed the topic with Marr as well in a podcast.

He describes the mobile device as “the virtual front door of the institution,” but he stresses that you can’t just leave that door propped open. “The credential that is the key to opening that door will reside in the campus card office,” he says.

When it comes to service delivery on the modern campus, Marr explains, “geographic boundaries of a campus are no longer the primary driver, mobile devices and applications have blurred these boundaries.”

He suggests that campus card administrators get immersed in the conversations about mobile on their campus. “Let IT know that campus card solution providers are moving the credential to the phone,” he says, “I am confident that will get their attention.”

In the video, Marr highlights several exciting mobile initiatives underway at campuses across the country including Stanford University and University of Washington.

To listen to the podcast, click the play button below:

HID, Arizona State pilot multiple handsets, carriers and apps on campus

HID, Arizona State pilot multiple handsets, carriers and apps on campus

As the Fall semester geared up at Arizona State University, something revolutionary was happening in one of the residence halls. Select students living in Palo Verde Main were no longer using their Sun Card to gain access. Instead they were using cell phones.

Compared to most residences, Palo Verde Main was already considered advanced in access control circles. For six years, contactless technology in the student ID card had granted access to the building. But in August, a group of students and staff became the first in the country to use smart phones equipped with near field communication (NFC) technology instead of keys or cards.

ASU worked with HID Global on the pilot. The company’s contactless iCLASS technology powers the student ID known as the Sun Card and HID readers secure residences, offices and labs throughout the Tempe campus.

Though the pilot came together rapidly, the spark for it was years in the making. “Three-years ago I began to notice a lot of press around NFC,” says Laura Ploughe, director of Business Applications and Fiscal Control for University Business Services at Arizona State University. “I mentioned it to my HID rep and about a week later he sent me news clip from ASSA ABLOY hospitality with a photo showing a phone opening a door.”

It was an “aha” moment. She realized the phone was the ubiquitous device that would really change things. “I stuck the news clip on my wall with a pushpin and it has been there ever since,” she says.

At a trade show this spring, Ploughe saw a demonstration of HID’s new iCLASS line based on its Secure Identity Object concept. Called iCLASS SE, short for Secure Identity Object-enabled, it allows the access credential to be stored on cards, fobs, phones and other devices. “It was a dream come true,” she explains. “I could see live what was under that pushpin on my wall.”

Ploughe told her contacts at HID that she would love to be involved if they needed a pilot location. “Never in my life did I think they’d say yes,” she laughs. But by early summer, agreements were in place and planning commenced.

“I thought we’d take a 24-week timeline for a pilot,” says Ploughe. “But the timeline was shortened when we began talking to stakeholders.”

Ploughe works in University Business Services. Among other things, the division oversees the Sun Card program and the Electric Door Access and Surveillance program. She approached her colleagues in University Housing for support, as they would be crucial to the success of the pilot.

“We looked at where it would best fit in the school calendar,” she says. “Housing agreed to participate but wanted to do it during early move-in to ensure there was no disruption to student learning.” That dictated an August launch, so a single discussion shortened the original timeline from 24 weeks to just eight weeks.

On Aug. 1 the hardware and equipment for the pilot was installed. Internal communications were sent to stakeholders including the police department and facilities to make sure they weren’t alarmed when news spread that cell phones were opening residence hall doors.

The following week HID Global staff trained campus technicians and the lock maintenance group.

On Aug. 10 new phones were given to the students and staff participating in the pilot. In all 32 participants – 27 students and five staff – were provided NFC-equipped phones to use as they lived life in and around Palo Verde Main.

The hall was not selected by accident. It houses many of ASU’s engineering students, individuals with an obvious technical acuity. “We picked Community Assistants (resident assistants) because they have single rooms and are both responsive and responsible,” says Ploughe.

As for the staff participants, Ploughe explains, “we wanted a couple of people from facilities to be able to test the system and we also chose staff from the residence hall to assist with technical support.”

“Because this was a pilot, we decided it would be good to have multiple brands of smart phones,” explains Deb Spitler, HID Global ‘s VP of HID Connect. Participants were outfitted with one of three handsets: RIM’s BlackBerry Bold 9650, Samsung’s Android (multiple models) or Apple’s iPhone 4G.

Handsets with embedded NFC functionality are not widely available so the pilot relied on microSD cards and sleeves for the NFC functionality. Three separate carriers – AT&T, Verizon Wireless and T-Mobile – were used for mobile services.

Two separate apps were used to carry the electronic credentials. The BlackBerry and iPhone users ran ASSA ABLOY’s Mobile Keys Application while Android users ran a mobile access application from HID.

Each participant received a fully provisioned phone with unlimited voice and text service. At the outset, the hope was to use the students’ existing smart phones. “We surveyed them to find out if they had a phone that we could enable with a microSD card,” explains Spitler. “There was a very small number that actually had a workable handset … well over half had a basic phone and not a smart phone.”

So the school and HID put new smart phones into all their hands. Because participants would keep the handset after the trial, Spitler says, they matched the mobile carrier and handset model to the individual’s current service. In that way, they could transition their new smart phone to their current carrier post pilot.

“We hoped this would help to engage them and show them that their participation and input to the pilot was important to us,” says Spitler.

ASU already had HID iCLASS readers across the campus and at key points in Palo Verde Main. But to accept the new NFC keys, readers needed to be upgraded to accept the company’s Secure Identity Object credentials. At six entrances, iCLASS SE readers replaced the existing contactless readers. Four new locations were also enabled with the SE units.

ASU already had HID iCLASS readers across the campus and at key points in Palo Verde Main. But to accept the new NFC keys, readers needed to be upgraded to accept the company’s Secure Identity Object credentials. At six entrances, iCLASS SE readers replaced the existing contactless readers. Four new locations were also enabled with the SE units.

Additionally, four individual rooms within the residence hall were equipped with an offline door lock from ASSA ABLOY’s Sargent line. These locks require the use of a PIN in addition to the credential on the phone.

To gain access, students present keys, cards or phones at as many as four separate points within the residence hall. A main entrance, a courtyard entrance, a wing door and finally a room door each are secured. Most of the students still required the key to gain ultimate entry to their room, but four participants used the phone at all entry points thanks to the Sargent locks.

“When a student approaches a door they click the icon on the smart phone to launch the app and then present it to the door,” explains Ploughe. For the pilot, the countdown was set to 30 seconds before the application closes.

“The sweet spot was different on each phone,” she says, referring to the ideal physical place on the phone to hold next to the reader for optimal use. “We put a Sparky emblem (ASU’s mascot) on back of each phone to make it easy and convenient.”

At the midpoint of the pilot, an initial survey of participants revealed promising results. Key questions pertained to training and support on devices, functionality of the application and comparison to the card in terms of convenience and speed. Other questions asked for suggestions to improve the current functionality and ideas for additional applications.

At the conclusion of the pilot, a second survey was conducted to address changes in perceptions over time. Have you changed your mind on things? Are you more or less happy with the functionality? Would you like to see the functionality continue to be supported on campus?

Results of these surveys will be released during a panel discussion on Monday, Sept. 19 at the ASIS conference in Orlando. Look for additional details here next week on the survey results.

The pilot concluded on Sept. 6. At press time, ASU was reviewing the survey data to determine next steps.

For Spitler, the pilot was a lesson in reality meeting new technology. “It enabled us to explore how people use mobile credentials and NFC in the real world,” she says.

That is the real value of a pilot. It forces stakeholders to forget their preconceptions of a technology and address how people actually live and work.

As Spitler points out, this is why it was great to have a number of different devices, readers and apps. “It gave us different feelings and that is what a pilot is all about,” she adds.

“It’s my hope that we do a secondary pilot,” says Ploughe. “Ideally I would like the smart phone to be the tool for everything. Lots of people are driving a mobile app to smart phones but there is some risk.”

She hopes that one outcome of these pilots and this user directed research is the establishment of some best practices. “Take care of the risk,” she explains, “and we can open up other applications.”

Ultimately, for ASU it’s all about student success. “The key is engaging them the way they want to be engaged – the same way they do with their friends and with the same tool that connects them socially,” explains Ploughe. “It means that we provide our services to students with devices like this or we have failed in helping them be successful.”