Card, mobile credential, payment and security

A day in the life of a typical college student involves an array of transactions, each relying on the campus credential. The student may:

In a recent article by Fred Emery, Senior Business Development Manager at TouchNet, he explains that this type of “transactional ease” requires a coordinated, integrated technology strategy between the card office, campus vendors, and the institution's student information system.

This level of transactional ease takes strategic planning and effort, and our campus card and transaction systems are central to it all

He outlines eight ways that an integrated card system streamlines operations and delivers significant benefits to the institution.

One key way is the system’s collection of actionable data.

“Connecting campus card technology to the student record system captures real-time data … that helps administrators improve student support and services,” he explains. “For example, using it to better schedule staff or optimize food preparation for peak times in the dining hall leads to improved student and guest experiences, reduced waste, and a better allocation of resources on campus.”

Improved efficiency is another key benefit.

Campus administrators are pulled in many directions and don’t have time to jump back and forth between multiple systems. An integrated campus ID system eases administrative tasks, centralizes reconciliation, and enables a single reporting source.

“Additionally, integration to the student information system can increase efficiency through automated data exchange, removing the need for many manual processes such as posting general ledger information or updating student accounts,” says Emery.

This level of transactional ease takes strategic planning and effort, and our campus card and transaction systems are central to it all.

To explore the other six benefits and consider how you can use them to promote your program to senior leadership and other on-campus entities, read Eight Advantages of an Integrated Campus ID.

Recent studies show a significant spike in anxiety, depression, and suicidal ideation among college students. In the 2020-2021 academic year, more than 60% of students met the criteria for at least one mental health condition.

Webinar: Transact + Talkiatry = accessible mental health services for students

Tuesday, September 19 at 1 pm EST

A Transact-sponsored webinar will explore how its new partnership with psychiatric care provider Talkiatry is working to address the escalating mental health crisis on college campuses.

The partnership gives students access to mental health services via the Transact eAccounts app students already use for an array of campus services and transactions.

Talkiatry uses virtual care to eliminate barriers to access. Its services are covered by more than 60 health insurance plans and provided by a team of more than 300 psychiatrists specializing in treating mental health conditions including anxiety, depression, PTSD, and more.

“With so many college students struggling with everything from loneliness and low self-esteem to depression and trauma from sexual assault, it’s vital school administrators have access to the resources to help (students) stay in school and successfully manage their mental health,” says Robert Krayn, co-founder and CEO, Talkiatry.

“Improving student mental health is a topic we are passionate about at Transact,” explains Nancy Langer, CEO of Transact. “By incorporating Talkiatry’s resources into our products, we’re empowering millions of students and families with the tools needed to manage mental health effectively.”

Join Transact Campus CEO Nancy Langer and Talkiatry co-founders Robert Krayn and Georgia Gaveras on Tuesday, September 19 at 1 pm EST.

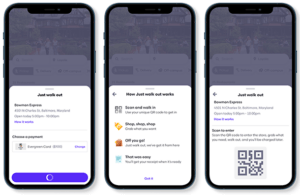

At a convenience store at Loyola University of Maryland, students are grabbing items and walking out of the store without checking out, scanning items at a POS, or seeing a cashier. Using Grubhub and Amazon’s Just Walk Out technologies, artificial intelligence, computer vision, and advanced sensors make it possible. The integration between the Grubhub app, already a fixture with Loyola students, and the Just Walk Out system is delivering a seamless and convenient solution for both students and operators.

Lyle Margerum, Director of Technical Operations, Grubhub Campus was on site at Loyola for the launch when we caught up with him to learn about this project and what it means to campuses across the country.

CampusIDNews: Thanks for taking time out from the events on campus. Can you tell me about the integration?

Grubhub: We have been talking with campus partners autonomous convenience stores for years. It is a challenging area to streamline with technology because it has always required cashiers. Just Walk Out provided an ideal the solution.

Early this summer we started doing the work with Amazon, and this week we delivered the first production orders.

Just Walk Out increases sales and brings value to students and the Loyola community. And it does it without the need to staff the location.

CampusIDNews: How does it work with Grubhub?

Grubhub: It is part of the normal Grubhub mobile ordering process. Just Walk Out appears as would any other on-campus dining location – say Chik-fil-a or a dining hall. The difference is that when you select Just Walk Out, there are no menu items to choose from within the app. They are going to choose their items when they enter the store. The user selects the payment method, and a QR code appears on the app’s screen.

The QR code is presented to the Amazon gate at the store, the light turns green, and the gate opens. Sensors and cameras determine which items are selected from the store shelves and track any unwanted items returned to a shelf. When shopping is complete, the user simply walks out the door. The transaction amount is charged to the meal plan account or selected payment method.

Before granting entry to the store, the system determines that there are sufficient funds in the campus account to enable a viable transaction. The Idea is to restrict a user with an ultra-low balance from overdrawing their account. If that does happen, the system could charge against a different tender or provide a report to the store operator to allow another collection process.

CampusIDNews: How did Loyola University of Maryland become your first partner for the new technology?

Grubhub: Loyola has been our partner since 2015, so we are leveraging a longtime partnership. They have been innovators on mobile ordering, kiosks, and other services for many years. Additionally, they have been talking with amazon and worked proactively to get this done.

Though they do have a transaction system provider, they did not want to introduce a secondary app just to support the identification of the student to the Just Walk Out system. Because the Grubhub app was already an integral part of campus life it made sense, and this integration just enhances our relationship with the student population.

CampusIDNews: Tell me about the rollout at Loyola.

CampusIDNews: Tell me about the rollout at Loyola.

Grubhub: I have been on campus this week for the launch, and it has been great. Loyola is already talking about future locations. The initial location is a convenience store operated by the campus dining provider Parkhurst. It is located in the bottom of one of the residential halls.

It offers the campus 24x7 retail availability that was not feasible in the past. Students have access to food and drinks, laundry detergent, and a range of other needed items right where they live. This increases sales and brings value to students and the Loyola community. And it does it without the need to staff the location.

CampusIDNews: What do you see for the future of Grubhub and Amazon’s Just Walk Out?

Grubhub: With our integration with Amazon in place, adding other campuses will be incrementally easier. We have ironed out kinks in the experience which will expedite both the planning and rollout process. Our second campus will launch in the next couple of weeks at Montclair University, and others are already scheduled for later in the Fall and Spring semesters.

For Grubhub, it deepens our value proposition with our partner institutions. We now cover the full range of a campus’ needs – mobile ordering, kiosks, POS, robot delivery, reusable container solutions, lockers – and now cashier-less retail.

Students at the University of Kentucky community can now use their WildCard Mobile ID on an iPhone, Apple Watch or Android device to access campus buildings, make purchases and more. Transaction system provider CBORD and access control partner HID Global worked with the campus to make the new system a reality.

Students download the Mobile ID from the App Store or Google Play using through the campus-branded CBORD GET app. Using the app they can download the mobile credential directly to their smartphone or watch.

“CBORD worked with the University of Kentucky to develop a plan to support mobile credentials throughout the WildCard program,” says Read Winkelman, Vice President, Sales, CBORD. “The university now joins many CBORD campuses already using mobile credentials successfully.”

Already, more than 100 institutions are embracing mobile credentials and this adoption will grow exponentially every year.

“We have supported NFC-based mobile credentials since 2012, and our customers process over 350,000 mobile credential transactions daily,” Winkelman adds. “With our partnership, customers see industry-leading rates of student adoption, which speaks to our ability to simplify the move for a seamless launch.”

Physical security is a key application for the university. The campus community relies on access control solutions from HID Global across campus administrative buildings, classrooms and residence halls.

“We are proud to partner with the University of Kentucky on the rollout of mobile credentials,” says Tim Nybolm, Director – End User Business Development, Higher Education, HID Global.

“Today’s student is ‘born digital’ and is looking for a convenient and exceptional user experience,” he adds. “With the use of mobile credentials, students have found a more convenient, efficient and secure way to access buildings and amenities on campus.”

Nyblom told CampusIDNews that Kentucky and many other campuses have embarked on a digital transformation journey using mobile technologies to elevate the student experience and increase security. He says, “already, more than 100 institutions are embracing mobile credentials and this adoption will grow exponentially every year.”

While student love the idea of mobile ID, some concerns always exist. What if I lose my phone? How do I get into my dorm if my battery dies?

Modern mobile ID solutions put these concerns to rest.

If a student misplaces their iPhone or Apple Watch, they can use the “Find My” app to lock and locate the device. Using Apple Wallet’s Express Mode, the mobile ID can be used without unlocking or waking the device. Even if the phone’s power is depleted, reserve power still enables the mobile ID to conduct transactions.

From a privacy perspective, a university release reassures students that Apple does not know when or where they use their Mobile ID, and transaction history is never stored on Apple servers.

Amy Surprenant, End User Business Development, HID Global, was onsite for the launch.

“Students were thrilled that they had student ID cards on their phones and no longer had to wait in a long line to get their IDs,” Surprenant says. “This mobile credential is not only convenient but provides increased security and enhances student experiences.”

For now, the university says students should still carry their physical ID cards. The new rollout is part of a phased approach, so some locations will still require a physical card.

The WildCard Mobile ID will be available to faculty and staff in the coming year.

Check out the WildCard online to learn more.

Days ago, the Colorado Department of Higher Education (CDHE) reported that a cyber breach may have compromised personal information for teachers, high school students and college students in the state from 2010 to 2020.

As reported in the department’s statement, they became aware of the ransomware attack on June 19, 2023. They took steps to secure the network and worked with third-party specialists to conduct a thorough investigation, restore systems and return to normal operations.

“An unauthorized actor(s) accessed CDHE systems between June 11 and June 19, 2023, and certain data was copied from (our) systems during this time,” says the Colorado Department of Education. “Our investigation has revealed that some of the impacted records include names and social security numbers or student identification numbers, as well as other education records.”

In 2022, 44 colleges and universities and an equal number of school districts were impacted by ransomware.

According to CBSNews.com, a CDHE spokesperson says the agency knows the source of the ransomware and confirms that it was not paid. The amount asked for was not disclosed.

Ransomware attacks in higher education are not uncommon. A study from malware research firm, Emisoft, reports that 44 colleges and universities were impacted in 2022. An equal number of school districts fell victim. In 65% of the cases, data was taken. The true numbers are likely to be higher as cyber attacks often go unreported.

Those that may have been impacted by in the Colorado breach include individuals who:

CDHE says it “is providing impacted individuals with complimentary access to credit monitoring and identity theft protection services through Experian for two years.”

Key management for contactless cards and mobile credentials is a hot topic in the higher ed campus card market. In this third segment of the HID Tech Talk series, HID's Tim Nyblom, Director of End User Business Development for Higher Education, and Nathan Cummings, Director of Sales Education for Higher Education, explore options for secure key management.

Listen in as we explore the pros and cons of owning keys, holding and securing keys internally on campus, and partnering with external key managers. The discussion will help clear up the confusion concerning this "key" security decision.

What is key management?

“Smart card and mobile credentials don’t just use a single key, they use a key set with multiple keys for multiple functions in the device,” says Cummings. “How those keys are generated, stored, used, distributed, and finally destroyed is the basis of key management.”

What does it mean to own your own keys? How do you build them, hold them, and protect them securely in a campus environment? Can you get the benefit of owning your keys but still rely on a partner to support your key management?

Click the video image at the top of this page to find out more.

Check out the HID Tech Talk Series:

Higher ed is facing a ‘demographic cliff.’ According to data from the U.S. Census Bureau, starting in 2025 there will be a steep drop in traditional the college-age population. The reason? Between 2007 and 2020, the U.S. birthrate fell nearly 20%, this will likely translate to fewer students, more competition, and tightening revenues.

The new CBORD Insights™ Student Experience Survey collected data from hundreds of students and administrators at U.S. higher education institutions. A primary finding was that on- and off-campus dining revenue is a major concern as campuses prepare for this declining enrollment. Findings suggest that automation and analytics are key to addressing the issue.

“Most colleges and universities operate their foodservice as a standalone enterprise that is expected to turn a profit year after year,” said Dan Park chief executive officer of CBORD. “Dining services typically represent a significant revenue stream, and the disruption of that income has been a top concern for higher education leadership since 2020, when nearly all residential schools closed in response to COVID-19.”

Departmental leaders ranked exploring new revenue sources as their top initiative, while higher ups ranked it second only to labor-reducing automation.

Staffing shortages and predicted declining dining revenues, find administrators turning to automation to maintain service levels and preserve dining revenue. Initiatives to automate dining operations, create frictionless foodservice, and expand dining options are underway at half the institutions surveyed.

According to the study, half of the respondents have invested in automation in the last two years, and more than half expect to in the next two years. Departmental leaders ranked exploring new revenue sources as their top initiative, while higher ups ranked it second only to labor-reducing automation.

Potential new revenue streams cited include:

Still, it will not be easy. Further stressing auxiliaries, respondents expect incoming students – accustomed to remote learning – to be less likely to live and dine on campus.

“COVID-19 caused us to reevaluate some major aspects of our financial model and has led to a shift in how we think about on-campus dining,” said Mike Henderson of the University of Tennessee at Knoxville. “We are seeing many opportunities to use mobile technology to collaborate with our surrounding communities to provide dining services.”

To learn more about the results of this survey and other areas covered beyond dining, click here.

So, Rich, we're just looking to understand more about the experience of working with Grover at Holy Cross as we shared.

So, if you, I know you stepped into working at Holy Cross when mobile ordering kind of was already up and running at most of the units.

So, do you want to share a little bit of history as to how things have gone and what things look like today?

Absolutely.

So, when I got here, I'd say about 80% of our transactions, if you want to call them that, were out of the residential dining location.

So, this has nothing to do with mobile ordering.

But it was too many people frequenting that one space.

There wasn't enough seating.

There was congestion.

Parents were complaining.

Students were complaining.

So, how do we get some of these folks, how do we get a better balance on campus?

How do we push them to some of the retail locations?

So, after a lot of thought, we decided we were going to change some menus around.

We were going to take a look at how we were doing mobile ordering.

We were going to make sure that we marketed that better for all the freshman students that were coming in.

And then we immediately realized that, wow, mobile ordering is starting to go up.

These students are starting to frequent the other spaces more.

We're making it easier for them to be able to get the products.

A conversation I recently had with a student was, we were talking about mobile ordering and the student's comment was funny.

He said, you've made it way too easy for us.

It's just so easy to get food and beverage any time now that you don't have to wait for it anymore.

That you can just be in a class or you can be in a locker room, you can be at your workout, you can place your order and you can just come and pick it up.

So, then what was happening was, as you know, the campus our POS system was just horrible here.

So, the campus wanted to change out the POS system and then part of that POS system they were talking to us about unlimited.

And then that's when I thought, okay, we're going to go unlimited, we're paying all this money for GrubHub.

The campus wanted to include the unlimited.

So, I gave Christy a heads up and thanks to GrubHub came back and said, well, we can do unlimited too.

So, that was great because now we didn't have to switch our students from GrubHub to another platform.

But then, you know, Christy just helped us so much with maximizing.

I really, Christy, you have so much to do with us.

Just helping us maximize the opportunities to just utilize the platform more.

So, we ended up switching one of our locations to mobile only.

We still had a cashier station off to the side just in case some of our older folks would come in.

We can still bring them up.

But a little bit more hidden.

No complaints.

We doubled the volume in that one location and the staff loves it.

So, there's no more of that.

Unfortunately, there's no more of that interaction.

I was just showing this to my wife recently that we go into Starbucks, which I always use the Starbucks app, but this time we didn't.

We go into Starbucks and I ask my wife to time it.

She's like, what are you doing?

I said, just time this whole thing.

She's like, what are you doing?

Just time.

So, we place the order, exchange our pleasantries.

They write on the cop.

They go through the whole process.

We bring the thing up on our car.

They scan it.

Two minutes.

Okay, two minutes.

So, that's two minutes of production that was lost.

So, our students are the cashiers.

Let those students actually go on their phone.

They're the cashier.

They do the whole transaction.

It comes out of their dining dollars, comes out of their credit card, meal plan, whatever it is.

Now we have a printer.

It prints a little sticker.

You put it to the cup.

How many drinks can you make in two minutes?

Four.

So, you think about how you're tying up that cashier.

Then we completely change the flow of one of our locations where we now have those, correct me if I'm wrong here, we have two TV screens.

The orders populate.

I think our staff just kind of swipe some as they're coming in.

But looking at the footsteps that they were taking, the steps that they were taking before compared to what they're doing now, everyone is virtually staying still now.

Our staff is staying still.

They got the order.

It comes up on the screen.

They work in their space.

They put it up on the counter.

There's a receipt.

There's a sticker.

So, Christie really helped us work through that whole thing.

Go to Dunkin' Donuts.

They're brilliant.

They have that totally figured out.

They're dialed in.

We have that dialed in now.

Starbucks is the same way.

So, it has maximized our efficiencies.

Our staff does not complain that they're doing double the amount of volume.

They're actually saying this is so much better because they're not running around anymore within the space where the cashier would have to hand off the receipt.

They would have to go and make the order as you can imagine.

So, it's just far more efficient.

So, then mid-semester, and I hate doing things mid-semester, our grill, one of our grills in retail actually, Christie, it was you.

We were talking.

You're like, why don't you just go with mobile order only at this location.

I was kind of sweating a little bit.

I'm like, you know what?

Yeah, we're going to do it.

So, I told the team.

I said, you know what?

We need a week.

Let's get our marketing to roll this out.

Let the students know.

You've got to give people a heads up.

They actually didn't listen to me, and they rolled it out the very next day.

And I walked into the location.

It's mobile only.

I'm like, what are you guys doing?

They said, what?

I said, for a week.

They're like, you did?

I'm like, yeah, I did.

And it was so smooth.

No student complained.

No customer complained.

There was no prior communication.

These students today, this is what they want to do.

They want to order from their phone.

They don't want to order in person.

And that location is now doing double the volume at that location.

Starbucks we proudly brew.

I was scared to death of putting it there all day long.

So, we're doing like two o'clock in the afternoon until five when we were the slowest.

And we doubled the volume in the afternoon.

Now we're doing it from the morning all the way to the night.

And the supervisor there, someone actually much older.

And sometimes our older folks have a hard time with technology.

She's like, I love this.

This is just so amazing.

So, being able to take that time away from the pleasantries, the ordering, typing everything in, grabbing someone's credit card or their card and swiping it, handing it back, and then making the orders.

Just so much more efficient.

So, I don't know if I'm answering your question.

I'm kind of all over the place.

Now you're doing great.

This is gold.

I feel like we got a whole article right there just from what you were saying.

It's amazing.

I mean, feel free to use me if you want to.

If you want to anything that I'm saying here, you can utilize it.

Thanks, Rich.

Yeah, we've got, I'm sure Rachel's mind is spinning with the thousand questions she wants to ask.

One question I have, I know you're talking about some of the locations like doubling in volume, that sort of thing.

Is that something you'd be able to pull some hard data on and we'd be able to use that in this article or case study or whatever it becomes?

Yeah, sure.

That's easy.

Okay, great.

Rachel, I'll let you go next because I've got a few too, but I'm sure you're spinning with questions.

Yeah, I mean, I feel like the first thing on my mind is you mentioned some upticks, doubling orders.

If you had to just really kind of simplify the biggest challenge and the biggest benefit, how would you just kind of frame that so I can use that as a lens while I process all the information you shared?

Yeah, I think the biggest challenge is talking people off the ledge, right, that we're going to do this and there's just this fear factor.

And myself included when you read this, when you read my article, I was really leery about mobile ordering 10 years ago when it all first got started.

How is this going to affect the staff?

Because I think people's head go, okay, we're not a restaurant.

We have this dupe machine, if that's what you want to call it, like in a restaurant.

If that thing just keeps going off and off and off and off, how are we going to keep up between the customers that are coming up in this dupe machine that is constantly going?

But it works.

You just have to trust it.

You have to trust the GrubHub partners, right, that we have.

You guys have seen it, seen this successful everywhere.

And the fact that we can take an entire location and switch it in one day with a completely different staff that has never experienced this before and see the sales double just within a few days, it just started to double.

It's just right there alone.

It's just you've got to trust the process.

You've got to trust the system.

The system works.

But I do like mobile order only even better.

I never thought that I would say that because it just takes those people out of the equation completely from walking up and ordering.

And our students love it.

Our community is completely fine with it.

I would say we probably have 100% of our students using it on a daily basis at least minimally once a day, sometimes twice a day.

And even our faculty and staff are fine with it.

So in the fall we'll have three locations, three entire locations that will be mobile only.

And that is just going to make us more efficient at those three locations.

Wow, that's awesome.

And in terms of obviously there may be some labor savings there or would you say you reallocated that labor because you were getting so many more orders that now you just were able to have more people fulfilling the orders instead of spending the time taking the orders?

Yeah, I never want to cut labor.

Everybody's different with that.

We're a non-profit institution.

We're not a for-profit like Sodexo or anything.

So what we did is we just took that same labor and just reallocated it.

And you were going to need it anyway with the uptick.

You're making it easier now so therefore you're going to get more orders.

You're going to need those people to now be kind of on that line preparing that food.

I wouldn't call it a labor savings.

It would be a labor savings I suppose if there was no increase in sales.

There's no increase at all in sales.

And you were doing the same exact volume.

But I don't think anybody that implements this and does it right would do the same level of sales.

I would say you're not doing it right or you're not doing a good job if you're actually doing the same level of sales.

I don't see how the sales couldn't go up no matter where you put this.

Yeah, that makes a lot of sense.

So really just focused on the increase in sales and then that creates a more efficient operation.

Yeah, and ultimately it's bringing down your labor percentage.

I would say that.

If I'm doing $400,000 at this location with $200,000 worth of labor but now I'm doing $800,000 in sales with the same $200,000 in labor, my labor percentage just went way down.

That's always from a financial standpoint.

That's always how I've been trained.

Everything is really percentages.

Yeah, definitely.

And then I know you mentioned a little bit about student satisfaction but just to drill into the student experience more.

Is there anything you want to add in terms of, like, I guess the fact that there's more sales means more students are using it and likely happy with it.

But just want to kind of talk about that angle a little bit.

Yeah, definitely.

And this is where I'm going to tell you a little bit about where you might get pushback from some people out there.

So this might even help with your writing, right?

Some folks are going to say, especially in the for-profit sector, which I did for 16 years with Compass Group, right?

They're going to say, well, they're on a meal plan and if they're utilizing that meal plan more, like here at Holy Cross, it's an unlimited meal plan in the residential dining, then they get eight meal swipes a week in the retail, and they're able to use GrubHub with those meal swipes, essentially not costing the students any additional money.

So, our participation rate is something that we really focus on and it has a huge impact on our financials.

Our participation rate is probably somewhere around 62%, roughly.

If I look at it right now and I do the numbers, I bet you we're closer to 85%.

Now, people who are in the business, especially in the for-profit world, are going to say, oh my God, that's costing you way more money.

Well, yeah, it is costing us more money, but what's happening is our satisfaction has gone up tremendously and I would say a great deal of that is because of GrubHub, but our credit card sales are now much higher also.

That's new money, that's new found money, that's real money.

So now that credit card sales and those additional transactions that are above and beyond the meal plan, that's new found money.

So now you have a lot more faculty, staff, and guests that are actually eating with us that were not doing that once before.

So, we drove, like our sales year on year have increased by, don't write an article on this and quote me on this, okay, please, but our sales have increased by $2 million, right?

Year on year.

So, a great part of that $2 million is we're able to get people through these locations quicker.

And a lot of that has to do with GrubHub, right?

So, but also it's costing us a lot more money because we're spending a lot more money on the meal plan food because the business participation is a lot higher.

So, the net net is yeah, we're still in a positive place and again, being that non-profit, we're beating our budget, we're making our budget, but we're feeding a lot more people.

And it's really, it's a win-win.

So, I've always believed even if you put GrubHub mobile ordering aside, that if you go for the quality and you go for the consistency and you drive the program to satisfaction, you're always going to get additional organic sales that are outside of that meal plan.

That's always worked out really well for me.

And now doing it the way we're doing it, having the kiosks available for those non-GrubHub app users, watching parents all the time, watching groups come in, they're using those kiosks, where maybe before they would not have ordered with us because it was just long student lines.

But now they can actually place the order and they can get a text message saying when it's ready.

So, it's just a total game changer.

Amazing.

Super, super helpful insights there.

Christy, are there any questions you want to ask?

Yeah, I do have a few.

I think you touched on this one already, Rich, but you talked about at the beginning of the call how your all-you-can-eat dining hall was really overloaded and that you're kind of trying to focus on this push towards retail.

You know, in your you mentioned like you've had a big increase in sales and everything.

Do you think you've just spread volume away from the all-you-can-eat to retail?

Or do you think, is it a true net increase?

Oh, it's a true net increase for sure.

So, yes it's 50% are at Kimball Hall versus that 80% of those meals, but it's not the same number, not even close.

I mean, it's $2 million of additional revenue in those transactions.

I think, I have the number, I don't have it in front of me, but it was a ridiculous number.

I want to say we served like 250,000 more meals year on year.

So, and we would not be able to do that without a mobile ordering platform.

We might have been able to push it by 50,000 meals or something like that, but certainly not. $250,000, 250,000 more meals.

And again, a lot of that's being driven by meal plan, but still, it just shows you how much more efficient and the capabilities by utilizing the platform.

And Rich, I know something we've talked about before.

Can you touch on a little bit how GrubHub helps you at peak meal period?

Yeah, no, absolutely.

So, what happened before, students break out of the class and they run to these locations, right?

Some, I would even say it's a bit of a safety issue, the way they go to these locations because they want to get there and they want to be able to order.

But what they're doing, of course teachers don't want to hear this, is they're ordering ahead of time in class.

So, our staff, instead of preparing the food in front of you when you get there, we're now spreading it out through a much larger duration.

And this is where the double of volume comes in, right?

If I've got 1,000 people coming at me, it's going to be a very slow process.

I have that same 1,000 people sending in those mobile orders 15 minutes, 20 minutes before they actually get there, then we're able to accomplish that.

They all come in, nobody's waiting in line, nobody's going to the cashier station, they're grabbing their food, they're walking away.

Some are staying, some are going.

Thanks, Rich.

I have two more questions for you.

Have you found on campus that any of the students or staff miss the daily interactions or anything or is everyone happier with things in this setup?

I would say happier, absolutely happier.

They still have that opportunity to break bread, if you will, in the residential dining location.

They can come in there, they can talk to the professional staff, they can place their orders there in that residential dining experience.

But really for that, and honestly, that is the busiest meal period now for Kimball, is dinner.

That's where our mobile ordering goes way down, is that dinner experience, where the students are sitting together, they are having that interaction, that conversation.

But let's face it, our students, especially 25% of our college is athletes, D1 division athletes, they are busy, they are super, super busy.

So every minute counts, and we're able to actually give them back.

I'd say we probably give every student back at least 15, 20 minutes a day by not waiting in line now, and that is very valuable. 15, 20 minutes a day really adds up.

I'm just making up numbers, but just kind of an idea.

Now they can go to the library, now they can work out a little bit longer, they can do other things.

So even this fall coming up, we're taking our concessions over, it was outsourced before, now we're doing an internal, and we're going to be doing these post, we're going to be doing a post-workout breakfast out of the athletic center.

So once you're done lifting weights, you're done with your cardio, whatever, swimming, whatever it is you're doing, you can now use Grubhub, you can order it ahead, and you're going to pick up your protein shake, your energy bites, whatever it is that you're looking for, and you grab it, and you go.

So again, trying to save the students even more time where they were working out, they had a walk from the top of the hill to the bottom of the hill, and Rachel, I'm sure you haven't been here before, call it a half a mile, right?

You're using a lot of time, and when I'm talking to the athletes, time is of the essence.

They're in there at 5, 5.30, 6 o'clock in the morning, they want to be able to finish their workout at 7.30.

If they can place that order, and they can grab it and run, and go back to their room, shower, change, go to their class, it's huge.

So our athletes are just beyond over the moon that we're able to give them this platform, and do this out of the athletic center come the fall.

And we're doing it, we're going to be doing it at night too, so all of the sporting games that are going to happen, the biggest complaint from our guests, because the college surveys them, I don't, is the long lines.

It's the long lines at the concession stations, now they're going to be able to order via the two kiosks that we ordered for that location.

They can use it from Grubhub Mobile, and we'll have some QR codes in the stands so they can be able to scan it.

We are eventually going to create a section within the luth, which is where the basketball is, and the ice hockey is, where we are going to deliver it to certain sections.

So let's call it a premium section.

Someone can scan that QR code, they can place the order, and we are going to have weight staff that is actually going to bring it to you.

Then we're going to do the same thing down at the football stadium at some point too.

So that's more of the future.

So every decision we have now, everything that we do, it's all about the mobile ordering.

I'm not blowing smoke, I'm telling you.

When I frequent all of these, I'm just so energized by it.

I can't believe I've been in this business my entire life, pushing 36 years now.

I know I don't look that old, but 36 years in this business, and this is like the biggest thing that I've ever seen in the business that is just a total game changer.

I walk in, I was down the cave, and you see these ice cream shops.

There's one called Sunday School, and it's insane to see the lines at Sunday School.

They had Grubhub, this would fly, they would probably quadruple their volume.

It took me 45 minutes, 45 minutes to place an order for ice cream at Sunday School and down the cave.

It is, once you have seen the light, isn't it hard to just not out in public, be like, there's a better way.

Have you seen the mobile order only stores for Starbucks now?

Have you seen it?

I couldn't believe it.

I was in New York City, and this is going back quite a few months, maybe six months ago.

And I'm like, oh my god, that's just the mobile order only.

You can't, there's no store.

But it was the coolest thing.

And then I saw one actually in Boston recently too.

Yeah, it just makes so much sense.

Of all brands, Chick-fil-A is actually trying it out in New York City right now too.

They're a brand that's totally known for the warm greeting, interactions, but I think even they as a brand are starting to see that a way to warmly greet your customers to allow them to order in the way that they want to order as well.

That is another way of warmth and kindness to your customer.

Right, right.

Well, a lot of my friends, colleagues in the business who work at other institutions, I'm like, you're an idiot.

You need to use, you've got to use this platform.

It's just amazing.

Hopefully they jump on board.

But it's amazing how people are just reluctant to change.

You know, I don't know how to do business that way, but you just got to do it.

And it works.

And you start slow.

So that would be my biggest recommendation to anybody.

Start slow.

Start at one location.

Don't go, maybe don't go all in right away, but you test the water.

Then you try a mobile order only.

Or maybe you do a pop-up event in the middle of campus somewhere and you just do mobile order only to see how it goes.

And then you kind of start there and then once you start to see it and you start to trust it, that's probably the biggest thing is trusting the process.

Because you don't want angry customers.

For sure.

Yeah.

What we see is like one of the biggest battles, one of the biggest hurdles to overcome is getting students to download the app.

Right?

Like, that's something that, you know, on your campus it's so critical that they download it.

It's like you're not going to be able to eat in several locations if you don't download it.

So because you all have gone so all in, so to speak, it almost makes it easy for you to talk to your freshman and say, hey, you've got to do this.

Right?

Like it's necessary to eat on campus.

And we work with several other campuses who work that same way too.

I'd say at the campuses that are more so dabbling in it, trying it at one venue, students don't really see the value in downloading an app when it's just one venue.

Right?

They might say, I'll just go to the one next door rather than sit here and download an app and mess around with that.

Good point.

Good point.

So it's interesting, it's kind of like those campuses that really dive in head first, students really understand the value of it because it brings so much value across the whole campus.

So that's kind of what we see.

How does that piece go with your freshman?

Like how do you share to incoming students the importance of downloading the app and getting set up?

Yeah, I mean, unfortunately, so much stuff is sent to them.

Actually, my son will be here very soon.

I already told him, I said, download the app.

And he's like, I need to download the app.

So these students, what's going to end up happening is we're going to message them, they're not going to read it, we'll have signs up, they're probably not going to read it, they're going to go to a location and they're going to go, oh, the only way I can get food here is to download it.

That's when they're going to do it.

So we need to make sure that we have some ambassadors out there, we will have the signage, but we know the first week or so, the retail locations are actually going to be slow because the students are going to be slow in getting that downloaded.

We know that residential dining, as I actually just talked about today with my team, we're going to be very busy in residential dining and then they'll slowly start to drift to those retail locations once they get that rub up figured out.

But we'll communicate with them, but everybody's communicating with them.

So they're overwhelmed when they first move in.

For sure.

And I feel like the overwhelm also leads to just go to the dining hall because that's easy and I don't need to start learning where the other locations are or how they work.

Exactly.

Yeah, that makes sense.

And something now that you have the kiosks too, and this is going to be your first back to school with the kiosks, I'd say other campuses that have a very similar setup to you where you lean into mobile ordering as the heavy way to do things and there's a couple kiosks around, you're going to see really long lines at the kiosks during peak lunch periods.

So the other campuses we work with with similar setups, they truly block out the first two weeks of the school year during lunch period to have a lot of their managers just go stand at the kiosk with the QR code and go download the app, download the app, download the app, just down the line just talking to the students because it's one of the most effective ways.

You don't have to get them to read an email, you can just talk to them and solve their problem while they're standing in it.

Absolutely.

That's our exact plan.

Yep.

Love it.

Absolutely.

Yep.

And the other thing too, I don't think you have on campus right now is we do have some of these signs that Melissa could order for you.

For your three mobile only venues just so you could have this kind of up near where the register would be.

Just to help students see the messaging.

I'd love that.

CR80News was onsite at last month’s Transact360, the annual Transact Campus user group conference. Great speakers, great networking, and a packed technology exhibit hall highlighted the three day event. Here are a few of the highlights from the expo:

Retransfer printers, direct-to-card printers and distributed enrollment and issuance were the topics on tap for Entrust Datacard. Product Marketing Manager, Martin Hoff, said that modern card issuance is about “busting the lines.”

Retransfer printers, direct-to-card printers and distributed enrollment and issuance were the topics on tap for Entrust Datacard. Product Marketing Manager, Martin Hoff, said that modern card issuance is about “busting the lines.”

In the past, if a printer went down it could shut down the issuance process. With distributed issuance and the company’s TruCredential solution, you simply route the job to another location. Putting the card issuance software on a server enables this distributed issuance and lets the campus enroll cardholders anywhere on campus, not just in the card office.

International students have added challenges when it comes to paying tuition at US institutions, and managing international payments is where Western Union thrives.

International students have added challenges when it comes to paying tuition at US institutions, and managing international payments is where Western Union thrives.

“We are fully integrated with Cashnet to help international students move money to pay tuition,” says Ben Kavalec, the company’s US director of sales.

Students make payments in their local currency and the institution gets paid in US dollars. The benefit for the student and their family is that they get preferential Western Union corporate rates for the transaction as it's a domestic payment for them rather than an international wire. If they went through their local bank to initiate the transaction, they would pay as an individual for an international wire at the highest rate.

Institutions also pay for receiving these international wires and the Western Union offering reduces these costs as well.

Access control readers that can consume both the mobile credential and the physical card were on display at the Allegion booth. The company’s AD and NDE reader lines both accept mobile credentials, and Allegion can help campuses accept both iOS and Android devices in PACS environments.

Access control readers that can consume both the mobile credential and the physical card were on display at the Allegion booth. The company’s AD and NDE reader lines both accept mobile credentials, and Allegion can help campuses accept both iOS and Android devices in PACS environments.

Mark Casey, Director National Electronic Sales, says the biggest change this year is that people are making decisions when it comes to mobile first. “People were talking at the 40,000 foot level about what mobile could do, but now its shifted to action – how do we it and who do we involve."

The mantra for access control provider Salto Systems has always been “data on card,” because they cleverly used the users’ cards to transport system-level data to their network of readers. Today that mantra has expanded to “data on phone,” as they recently rolled out mobile credential acceptance within their large deployed infrastructure at the University of Santa Clara.

The mantra for access control provider Salto Systems has always been “data on card,” because they cleverly used the users’ cards to transport system-level data to their network of readers. Today that mantra has expanded to “data on phone,” as they recently rolled out mobile credential acceptance within their large deployed infrastructure at the University of Santa Clara.

Jeff Wood, National Manager OEM at Salto, explains that their readers connect wirelessly not to find out if a cardholder has access to a door (they already know that based on data held on the card itself), but rather for managing system functions and enabling lockdown situations. “Data on card or data on phone still works with power outages as our locks are battery powered,” he says.

It’s also a cost effective install. “In a place like New York City, the end user cost could be $8,000 per door for a wired solution, but this gets that down to less than $1,000 and a five-minute install.”

A wide variety of biometric readers – from basic fingerprint-only readers to multi-factor devices and even contactless scanners – are serving higher ed installations thanks to IDEMIA.

The MorphoWave Compact is an option that is growing in popularity for use in unlimited access dining locations, rec centers and libraries, says Dave Gershenson, National Sales Manager for IDEMIA.

Gershenson has also seen a growing trend of scanning in and scanning out of academic facilities like libraries, as well as other on-campus locations. “In athletics, biometric access has become a recruiting tool to show off facilities to potential athletes,” he says.

Many Transact readers and devices are made by a leading contract manufacturer that also happens to do good for our society.

Many Transact readers and devices are made by a leading contract manufacturer that also happens to do good for our society.

PRIDE Industries employs 3,400 people with disabilities across 16 states. That is more than half PRIDE’s workforce, so it's not just a PR move, but rather a core part of the company’s socially responsible mission.

According to Mike Douglas, PRIDE’s General Manager, PRIDE gives people a sense of purpose and gainful employment and that improves lives. Next time you use one of your Transact devices on campus, feel good knowing that lives were changed in its creation.

“We like to support our partners, and Transact360 and other user group events provide a great opportunity to connect and engage with the market,” says Dawn Thomas, Executive Director, NACCU.

“We like to support our partners, and Transact360 and other user group events provide a great opportunity to connect and engage with the market,” says Dawn Thomas, Executive Director, NACCU.

At the booth, Thomas, alongside membership engagement manager, John Ogle, met with a number of campus administrators – both members and potential members – to share association plans and learn what campuses need in terms of support.

NACCU provides both in-person and virtual educational opportunities throughout the calendar year targeted directly at higher education card and identity professionals.

The sleek turnstiles from Alvarado would make a beautiful addition to any campus facility, and CooperCraft has installed them for Transact and other campuses.

The sleek turnstiles from Alvarado would make a beautiful addition to any campus facility, and CooperCraft has installed them for Transact and other campuses.

The optical barrier turnstiles are ideal for rec centers, student housing, dining halls and libraries, says Dan Gardner, Security Sales for Alvarado. He says that the turnstiles detect wrong-way entry and enforce one-to-one access by eliminating tailgating. It can also reduce staffing needs by removing the human the need for a person to scan ID cards at dining and other locations.

“We have turnstiles at Georgia State University providing data for their analytics on rec center usage,” explains Jerry Cooper, CooperCraft CEO. “They are great looking pieces and they can be customized with etching for each institution."

This spring, a new reader will join the Assa Abloy family that includes a keypad for situations when dual authentication is desirable.

This spring, a new reader will join the Assa Abloy family that includes a keypad for situations when dual authentication is desirable.

According to Tyler Webb, Assa Abloy Regional Manager, some campuses are seeking added security for residence halls. “We are hearing from institutions that are beginning to question if a single credential is enough for securing living spaces,” he says. "This new reader is designed to address that need."

CR80News was onsite at the 40th annual CBORD User Group Conference (UGC 2019) this week. There were many highlights, great educational sessions, and a packed technology exhibit hall. Here are a few of the highlights.

The sleek and secure turnstile from Smarter Security equipped with IDEMIA’s MorphoWave hand scanner was a hit with UGC attendees. The stainless steel and glass unit would look great in any high-end facility. It features anti-tailgating sensors with various alarms to warn staff of suspicious activity. According to Dave Beckwith, CBORD's product manager for integrated security, the primary use case is all-you-can-eat dining facilities. New firmware updates to the MorphoWave biometric scanner increase throughput by 20% and raise the number of patrons that can be enrolled in the unit from 20,000 to 100,000. The system is fully integrated with CBORD’s CSGold platform.

The sleek and secure turnstile from Smarter Security equipped with IDEMIA’s MorphoWave hand scanner was a hit with UGC attendees. The stainless steel and glass unit would look great in any high-end facility. It features anti-tailgating sensors with various alarms to warn staff of suspicious activity. According to Dave Beckwith, CBORD's product manager for integrated security, the primary use case is all-you-can-eat dining facilities. New firmware updates to the MorphoWave biometric scanner increase throughput by 20% and raise the number of patrons that can be enrolled in the unit from 20,000 to 100,000. The system is fully integrated with CBORD’s CSGold platform.

Nextep Systems showcased a series of kiosks for ordering and payment for CBORD food service locations. According to Brian Machiniak, Senior Relationship Manager for Nextep Systems, “self-service at the university level is a demand now.” The company’s range of self-order solutions support multiple methods for order and pay, and Machiniak stresses that flexibility is key because even on the same campus different dining operations require different setups. Nextep has been building self-service kiosks for 15 years, and Machiniak says clients typically see a 15% increase in the average ticket price due to the up-sell capabilities of the devices. Nextep Systems is part of the Xenial group of companies owned by Global Payments.

Nextep Systems showcased a series of kiosks for ordering and payment for CBORD food service locations. According to Brian Machiniak, Senior Relationship Manager for Nextep Systems, “self-service at the university level is a demand now.” The company’s range of self-order solutions support multiple methods for order and pay, and Machiniak stresses that flexibility is key because even on the same campus different dining operations require different setups. Nextep has been building self-service kiosks for 15 years, and Machiniak says clients typically see a 15% increase in the average ticket price due to the up-sell capabilities of the devices. Nextep Systems is part of the Xenial group of companies owned by Global Payments.

At the CBORD UGC event, Assa Abloy showed a compact version of its Aperio wireless locks that connect to mailboxes. The solution enables campuses to distribute mail to a secured box in a bank of mailboxes and restrict access to only the appropriate student ID card. Jim Primovic, Assa Abloy’s Director of Sales for Campus Electronic Access Control, demonstrated the solution and hinted at a major campus installation underway now.

At the CBORD UGC event, Assa Abloy showed a compact version of its Aperio wireless locks that connect to mailboxes. The solution enables campuses to distribute mail to a secured box in a bank of mailboxes and restrict access to only the appropriate student ID card. Jim Primovic, Assa Abloy’s Director of Sales for Campus Electronic Access Control, demonstrated the solution and hinted at a major campus installation underway now.

It looks like a glowing hockey puck affixed to a washer or dryer, but the Washlava device indicates when the machine is available, in use, or reserved by another user. Students interact with the laundry solution via a mobile app, reserving and paying for cycles. If they are standing in front of a machine, Bluetooth communication from their phone to the puck handles the transaction. They can also use the app to reserve a machine from their dorm or other location, locking it down for a specific number of minutes. According to Washlava's Hailey Hendrickson, MIT students pay for laundry cycles using their ID card's TechCash via MIT's CBORD system.

It looks like a glowing hockey puck affixed to a washer or dryer, but the Washlava device indicates when the machine is available, in use, or reserved by another user. Students interact with the laundry solution via a mobile app, reserving and paying for cycles. If they are standing in front of a machine, Bluetooth communication from their phone to the puck handles the transaction. They can also use the app to reserve a machine from their dorm or other location, locking it down for a specific number of minutes. According to Washlava's Hailey Hendrickson, MIT students pay for laundry cycles using their ID card's TechCash via MIT's CBORD system.

Crash bars are the metal locking mechanisms that span the width of many public access perimeter doors. Von Duprin is an industry leading provider of crash bars supplying 70% of the units in the higher education market, says Jeff Koziol, business development manager, campus software partner at Allegion. Allegion developed a retrofit kit for the popular crash bar that greatly improves campus safety. In normal operation, a staff person visits these doors and unlocks them so that students have unfettered access during normal operating hours. This unlocking process is known as “dogging” the doors. At the end of the day, the staff member goes back and “undogs” the doors, returning them to their locked state. Access control readers then require card access for entry. With the Allegion retrofit kit, Koziol explains that the undogging process can be automated such that many doors can be relocked from a central location. CBORD has integrated this new Allegion feature into CSGold.

Crash bars are the metal locking mechanisms that span the width of many public access perimeter doors. Von Duprin is an industry leading provider of crash bars supplying 70% of the units in the higher education market, says Jeff Koziol, business development manager, campus software partner at Allegion. Allegion developed a retrofit kit for the popular crash bar that greatly improves campus safety. In normal operation, a staff person visits these doors and unlocks them so that students have unfettered access during normal operating hours. This unlocking process is known as “dogging” the doors. At the end of the day, the staff member goes back and “undogs” the doors, returning them to their locked state. Access control readers then require card access for entry. With the Allegion retrofit kit, Koziol explains that the undogging process can be automated such that many doors can be relocked from a central location. CBORD has integrated this new Allegion feature into CSGold.

Around the world and on our campuses, the war against single use plastic is being waged. To-go containers from campus dining locations are a prime campus target. OZZI’s system of reusable containers and collection kiosks is already helping 90 colleges and universities eliminate waste and save money. “One OZZI container can replace 300 single use containers,” says Tom Wright, OZZI CEO. “An OZZI container costs less than $5 while each single use container costs 20-30 cents.” Campuses save money and help the environment. Typically a student redeems a token for a clean container and receives a token back when they return a dirty container to an OZZI kiosk. At the UGC event, OZZI demonstrated how CBORD has created a virtual token stored in the student card system, eliminating the need to keep track of physical tokens.

Around the world and on our campuses, the war against single use plastic is being waged. To-go containers from campus dining locations are a prime campus target. OZZI’s system of reusable containers and collection kiosks is already helping 90 colleges and universities eliminate waste and save money. “One OZZI container can replace 300 single use containers,” says Tom Wright, OZZI CEO. “An OZZI container costs less than $5 while each single use container costs 20-30 cents.” Campuses save money and help the environment. Typically a student redeems a token for a clean container and receives a token back when they return a dirty container to an OZZI kiosk. At the UGC event, OZZI demonstrated how CBORD has created a virtual token stored in the student card system, eliminating the need to keep track of physical tokens.